2026: The year of scarcity

It is hardly an exaggeration to say that the primary driver of equities year-to-date has been a scarcity trade, most notably in oil and AI infrastructure.

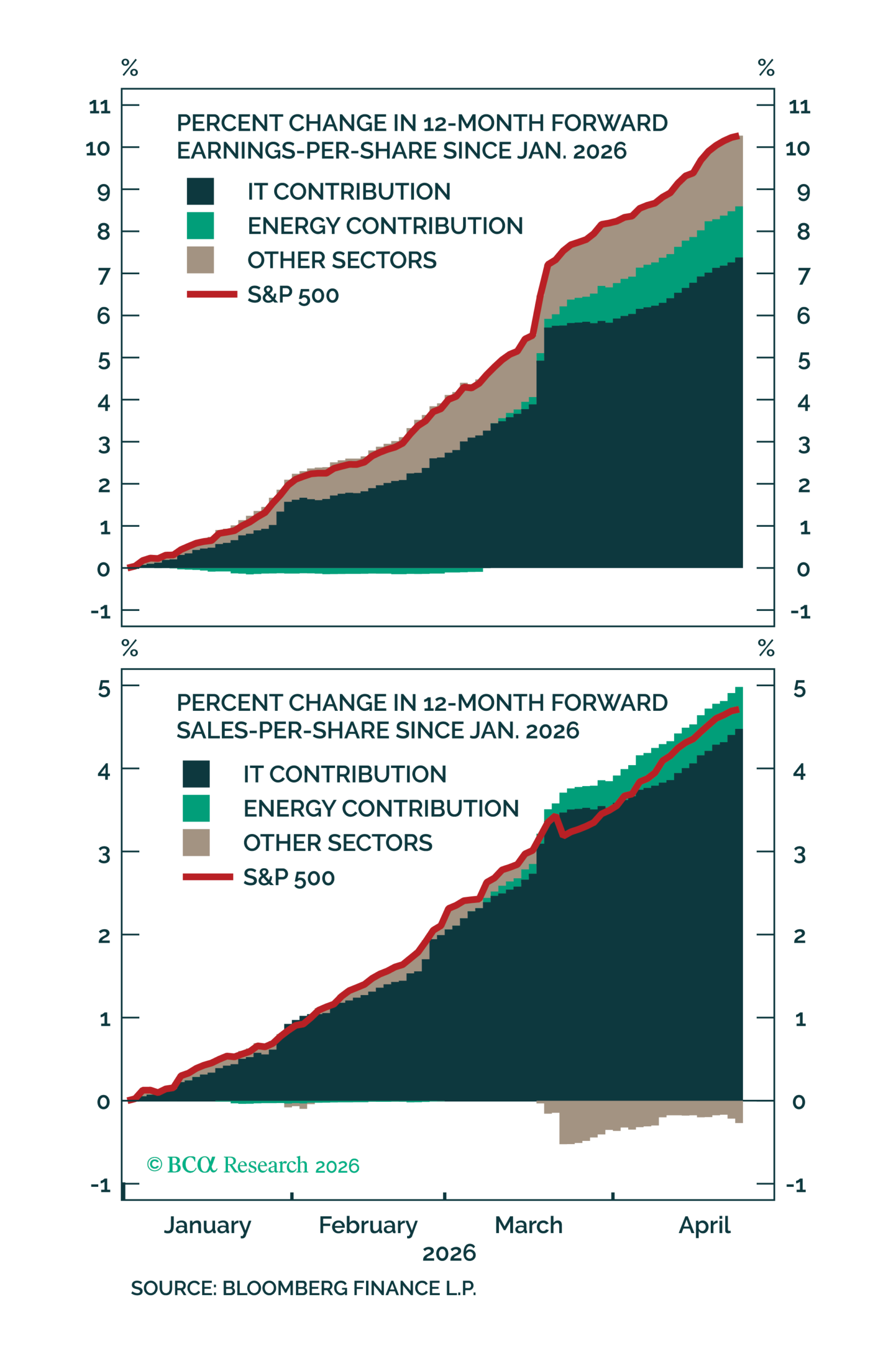

Figure 1 – Energy and IT have been the main drivers of upward revisions to earnings and sales estimates

S&P 500 profit margins remain near record highs. Since the beginning of 2026, forward 12-month EPS estimates have increased by 10.3%, while forward sales-per-share estimates have risen by 4.7% – see Figure 1.

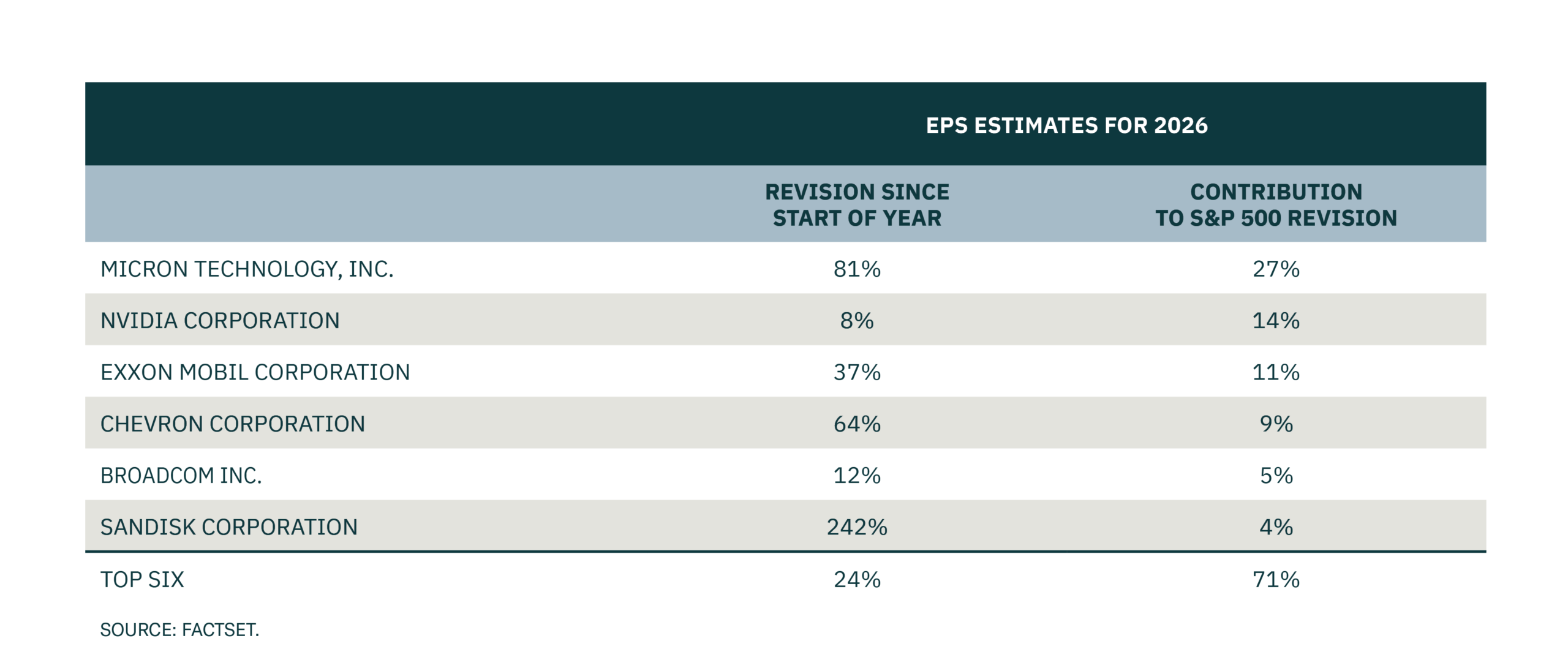

Figure 2 – Only a small number of companies have actually driven the upward revisions to S&P 500 earnings estimates for 2026

Almost all of the increase in forward earnings and sales estimates has been driven by just two sectors: Energy and IT. In fact, more than 70% of the increase in S&P 500 EPS estimates for calendar year 2026 has come from just six companies: Micron Technology, NVIDIA, Exxon Mobil, Chevron Corporation, Broadcom and SanDisk – see Figure 2.

The oil must flow

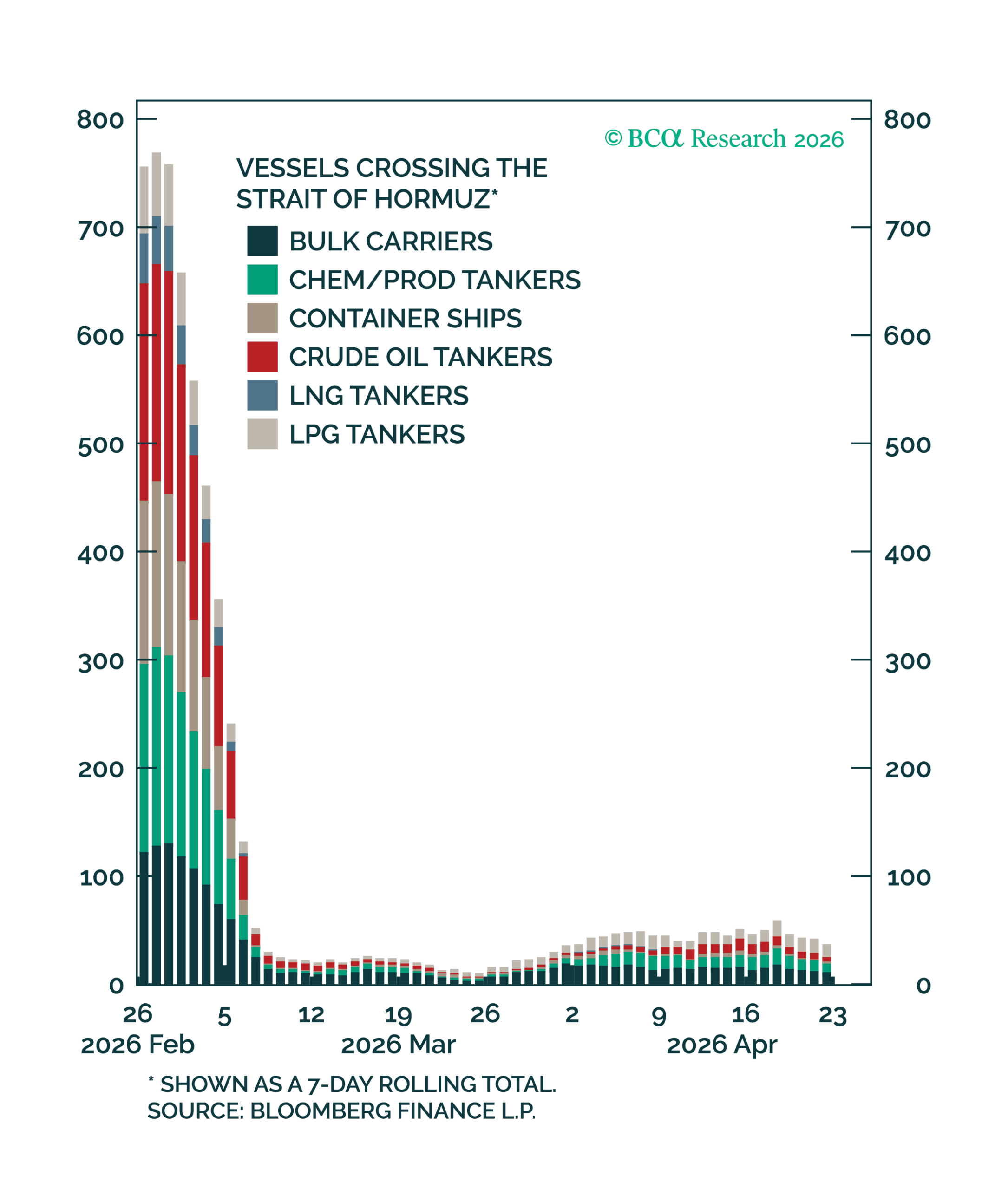

Figure 3 – There has been very little recovery in freight travel along the Strait of Hormuz

The oil trade has been pegged to the progression of the US-Iran conflict, which remains mired by uncertainty despite the many “ceasefires” that have been announced. Ten weeks into what President Trump had described would be a two-week “excursion”, ship traffic through the Strait of Hormuz remains well below pre-war levels – see Figure 3.

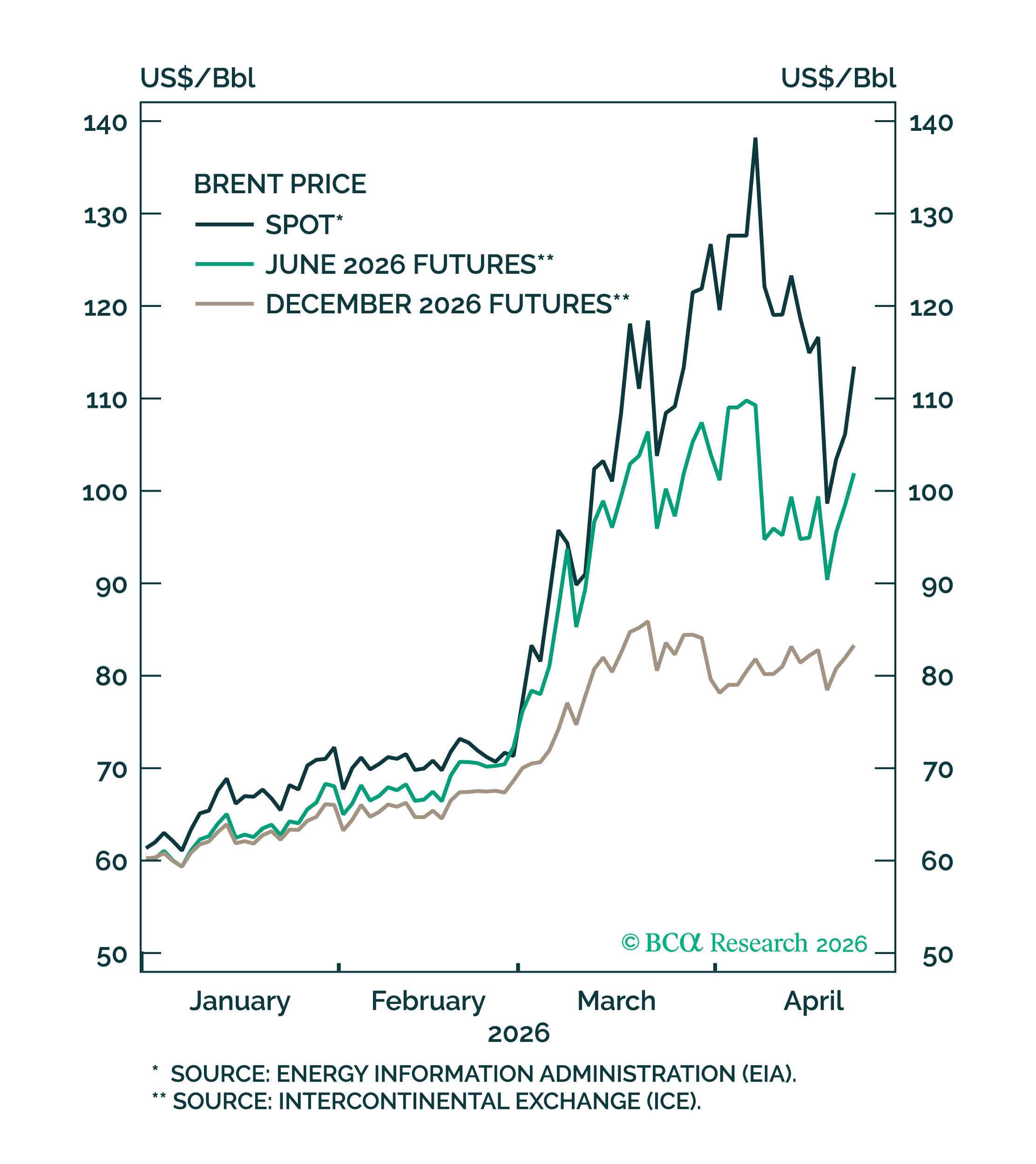

Figure 4 – Brent crude contracts for year-end delivery remains at elevated levels

The scarcity of Middle Eastern oil has lifted EPS estimates for US energy companies, with December 2026 Brent oil contract still trading +40% above where it did at the start of the year – see Figure 4.

Looking beyond the next few years, the odds are high that today’s oil shortage will fade. However, the geopolitical flashpoint has still spurred a debate on the near-term economic effect on consumption. A prolonged closure of the Strait of Hormuz, or even sustained below average freight travel, will eventually become a logistical nightmare for the subsequent cogs of the economy. Factoring in the transport lag, jet fuel will continue to run low and flights/commercial travel cancelled. Helium will become hard to find, leading to semiconductor production becoming more expensive and MRIs harder to obtain.

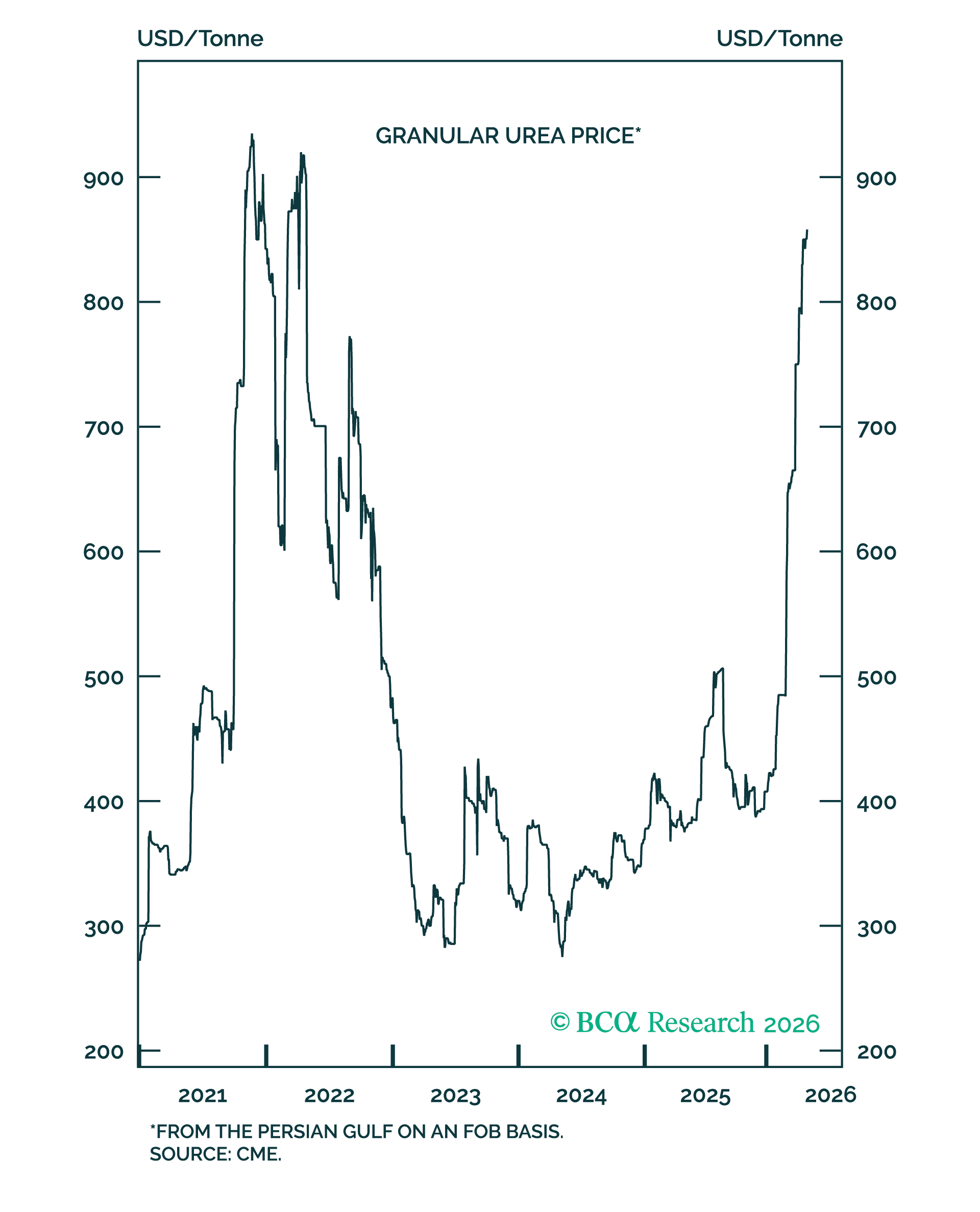

Figure 5 – Rising food prices is almost a certainty following fertiliser costs reaching past peaks

Additionally, fertiliser production will slow, and crop yields will subsequently fall. We have already seen important fertiliser products such as granular urea skyrocket in spot price since the outbreak of the US-Iran war, mirroring its past peak when Russia invaded Ukraine – see Figure 5. We can expect food prices to continue increasing, and thus both headline and core inflation to remain stubborn if no ultimatum on the Strait is reached.

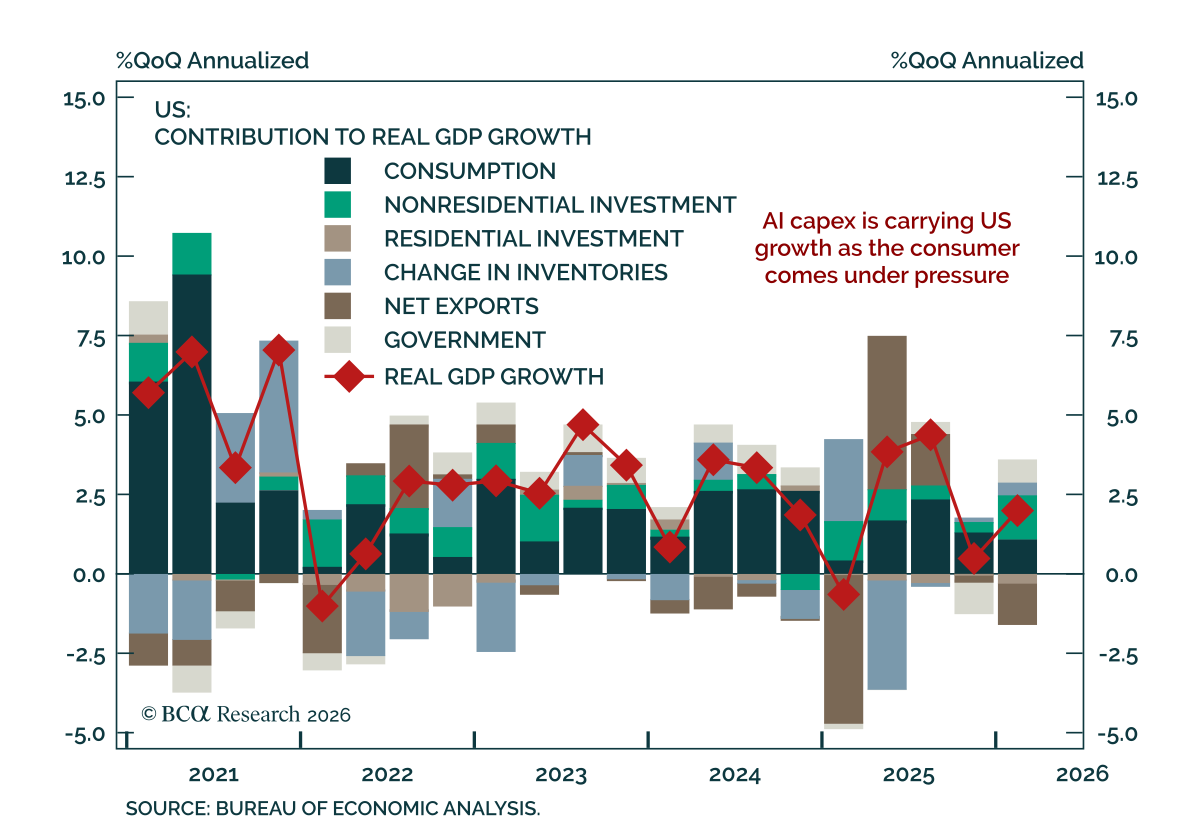

Figure 6 – US growth is increasingly being supported by AI-driven capital expenditure as broader demand cools

With the risk of oil-driven supply-shock inflation rising, the Fed is increasingly at risk of being trapped in a stagflationary environment, limiting its ability to justify rate cuts in the near term. Advance Q1 GDP came in slightly below expectations, expanding at a 2.0% annualised q/q pace versus 0.5% in Q4. Consumption growth moderated, while non-residential investment strengthened, largely driven by continued AI infrastructure buildout – see Figure 6.

The latest ISM readings corroborate the concern of a stagflationary outcome, showing flat headline growth alongside weakening underlying activity and rising price pressures, with the PPI surging to its highest level since 2022. Taken together with prior regional surveys, the data suggest softening momentum on growth but increasingly persistent inflation.

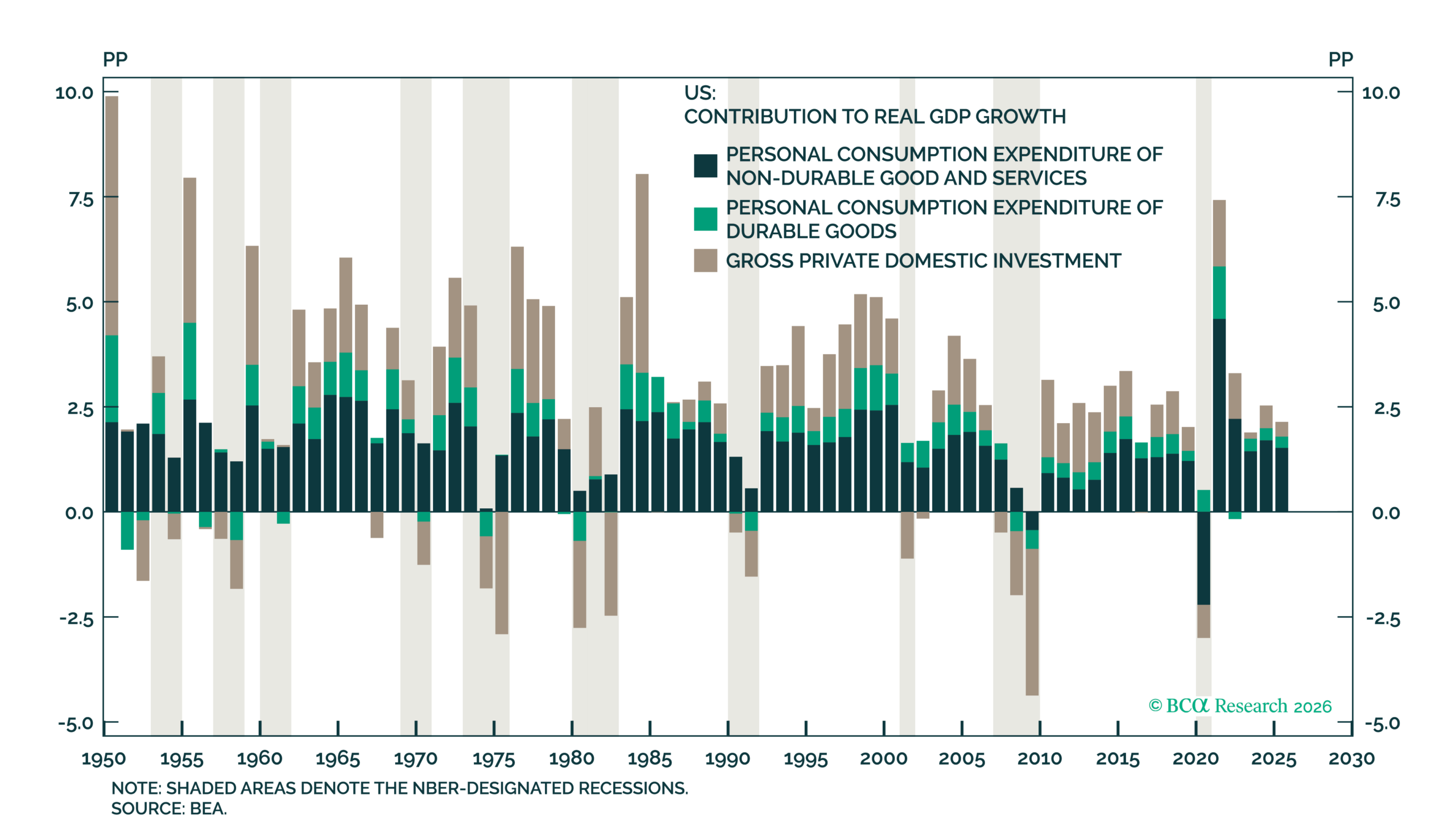

Figure 7 – Investment spending growth has typically been the primary driver of fluctuation in growth

The recent trend in GDP growth has shown that AI capital expenditure (“capex”) has undoubtedly become the lynchpin of economic activity. However, this is not as unique as it appears at face value. While the US is a consumption-driven economy (almost 70% of GDP is accounted for as consumption), the most important driver of economic has arguably always been the investment side, with gross private domestic investment being the only material component that fluctuates both in magnitude and direction of growth – see Figure 7. A large portion of consumption is anchored by the non-discretionary purchases of households, such as food and rent. The highly cyclical share of consumption, such as durable goods, is the smaller piece of the pie. Despite accounting for 60.8% of GDP, the fluctuation in services and non-durable consumption has only had a material impact in causing a technical recession during the pandemic (FY2020), when lockdown restrictions physically forced people to stay at home.

Deus (cap) ex machina

US GDP growth has increasingly depended on the “deus ex machina” of AI investment spending. Despite unresolved conflicts, growing input costs, uncertain demand outlooks, and a pressured US consumer: AI investment has remained undeterred, serving as an exogenous saving grace. Over the past 12 months, the hyperscalers have by themselves invested over $400 billion into data centres, equivalent to the GDP of South Africa. AI capex has effectively become the business cycle.

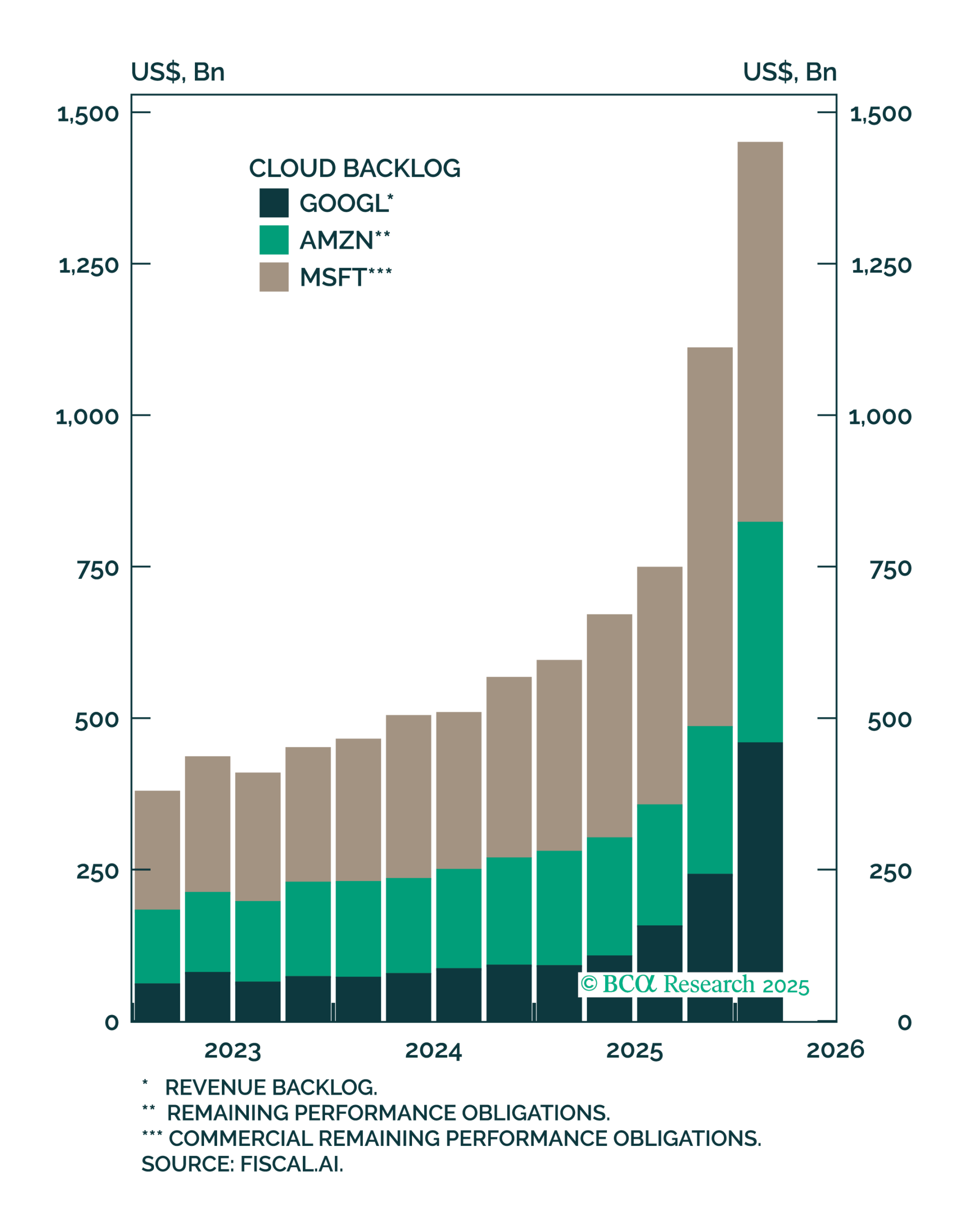

Figure 8 – For all intents, AI demand still technically exceeds supply

A fair response to the AI buildout being the economy’s saving grace is that this cannot continue forever. In the long run, firms will only commit to further capex when they are confident that demand will materialise to absorb the resulting supply. Right now, compute demand for the three major cloud providers (Alphabet, Microsoft and Amazon) has caused their respective backlogs to explode. Remaining Performance Obligations (“RPOs”) for just these three companies have increased from $596 billion in Q1 2025, to $1.5 trillion in the first quarter of this year – see Figure 8.

Building Agent Smith

The reasoning for this second wind in AI equities is supported by a new transmission channel for AI demand to funnel through. It bears mentioning that this also means that the original bear case for AI valuations is not as clear cut as it used to be. Previously, we described how the plateauing of marginal utility gained per cost to train would form a ceiling on AI valuations. As the latest generations of LLMs get released, the incremental innovation would diminish and hyperscalers would no longer have the incentive to increase their compute capacity for an immaterial gain in new knowledge. An abrupt decline in capex, and the economy with it, would follow.

The AI trend has since gained new legs, namely via the advent of agentic AI. Mechanically, the focus of the AI trade has rapidly shifted away from model training (the creation of new knowledge) toward model inference, where the emphasis is on efficiently applying established knowledge. Agentic-based inference maximises this efficiency, but is highly intensive in token usage versus the general prompt-and-reply framework of an LLM like ChatGPT or Claude. For agentic systems like OpenClaw to provide its value, the model repeatedly plans, executes actions, and refers to past context. This requires magnitudes more compute.

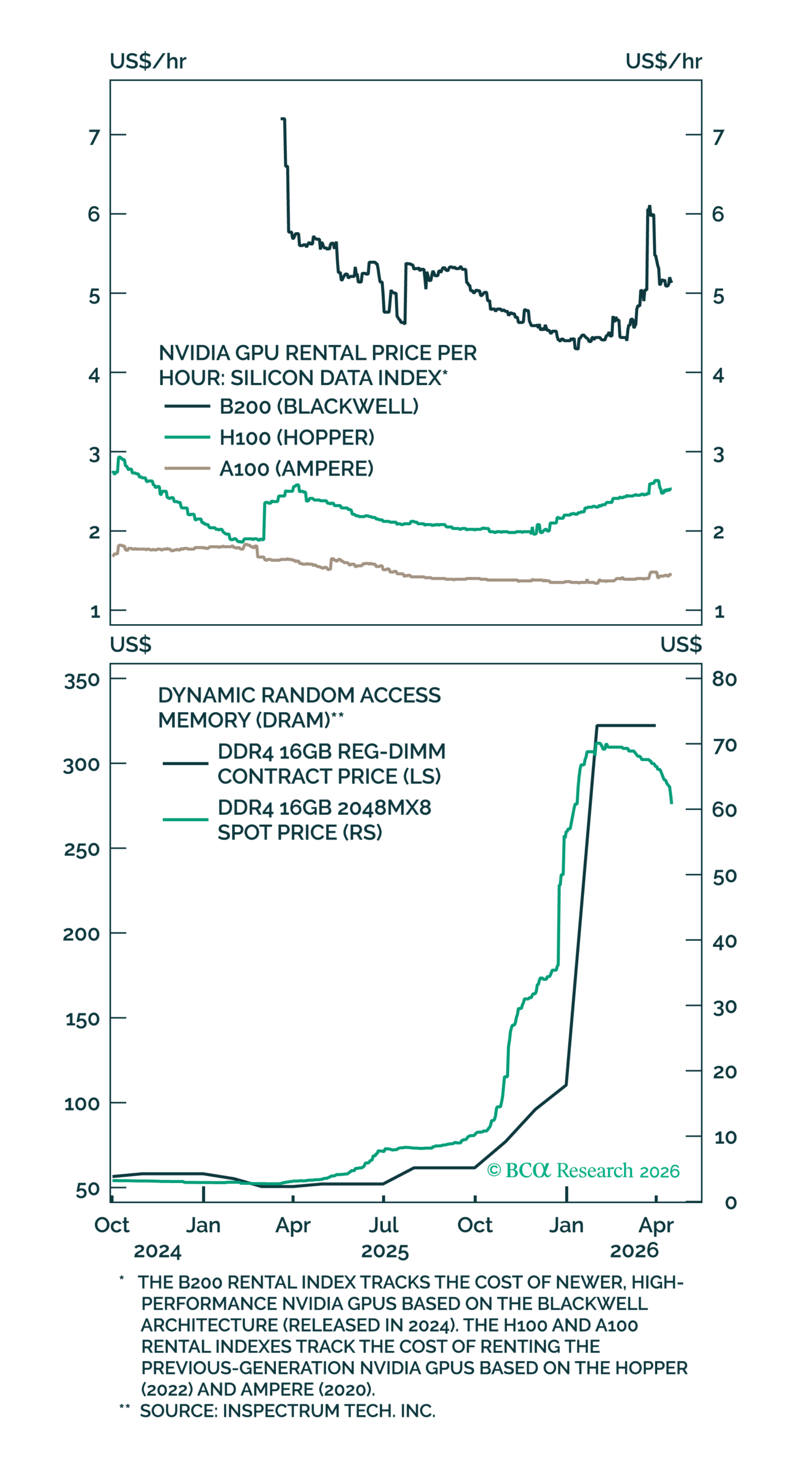

Figure 9 – Although GPU rental rates and memory spot prices have eased from their highs, they remain elevated

The excitement around agentic AI has reignited the fire, with the hypothetical demand outlook exceeding the feasible compute buildout once again. Parallel to this, Nvidia’s next generation chips, such as the Rubin R100, are guided to be built with inference needs as the priority. High-Bandwidth-Memory (“HBM”) chips, are vital for the large contextual needs of AI agents, and have become the bottleneck now. As a result, memory prices (and GPU rental rates alongside this) have skyrocketed – see Figure 9.

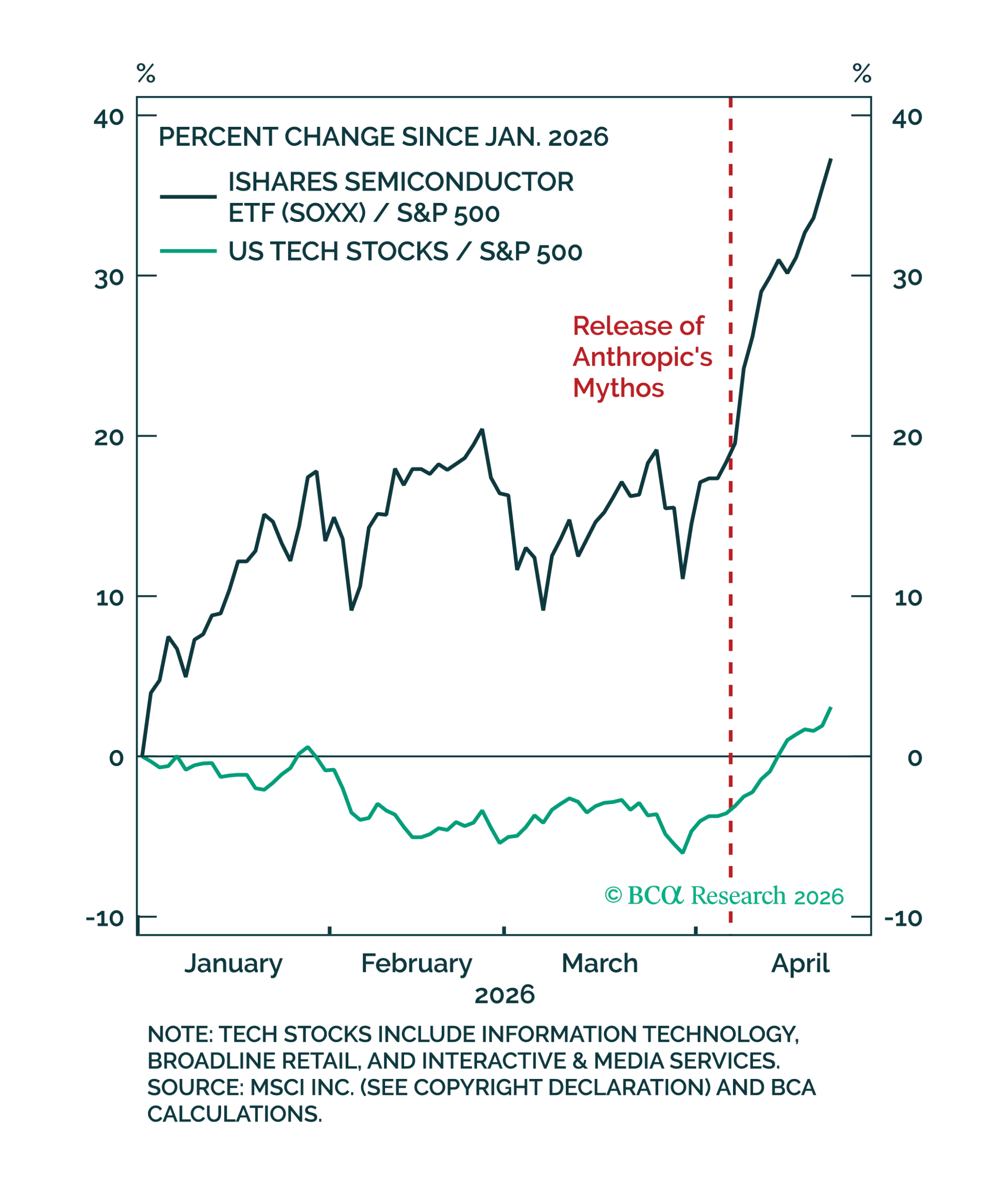

Figure 10 – Following stagnant innovation in prior LLM releases, Anthropic’s Mythos has reignited the fervour in the trade

It remains too early to determine whether this trend represents a durable shift or merely a passing fad. But without an exogenous shock, an AI bubble burst appears unlikely in the near term. Momentum in data-centre construction remains strong, with many AI-linked equities breaking new all-time highs. The rally in semiconductor shares kicked into high gear after April 7th, the day that Anthropic announced its Mythos model. Since then, the SOXX ETF (semiconductor companies) has risen more than 30% – see Figure 10.

Investment takeaway

Consensus expectations currently imply exceptional earnings growth through 2026, with S&P 500 operating EPS projected to rise roughly 20% year-over-year across each remaining quarters of the year. While the growth so far may initially appear right-tailed, earnings are historically volatile and similar surges have occurred around major business-cycle inflection points.

However, if the consensus earnings forecasts through till mid-2027 are realised, this cycle will become a clear outlier, with mature-cycle earnings growth materially exceeding that seen in prior long-duration expansions. This leaves the 2026 equity outlook heavily dependent on the continued profit growth thesis, particularly in AI infrastructure. The key risk is that any slowdown or stumble in agentic AI enthusiasm could still spell a deadly outcome, and we would be back at square one in bubble talk.

If you are interested in finding out more about how cognisance of the macroeconomic backdrop impacts our investment decision making process, connect with Integrity Asset Management and let us help you navigate your investing journey.

For more information on this synopsis or to discuss solutions provided by Integrity Asset Management, please contact us at:

Tel: (021) 671 2112

Cell: 072 513 2684 / 084 601 1025

E-mail: nic@integrityam.co.za / herman@integrityam.co.za

Source: Bloomberg, 30 April 2026