The US, at a glance

As we head into November, it is worth considering the impact of two key developments, namely 1) the US-China trade truce, and 2) the latest Fed rate cut.

1. A US-China trade truce

The United States and China have agreed to pause their trade dispute for a year. The arrangement includes a suspension of new restrictions on rare earth exports, a notable component of China’s trade – see Figure 1. Additionally, permission was granted for some blacklisted Chinese technology firms to buy chips through subsidiaries, and small adjustments to tariffs linked to fentanyl-related goods. China has also indicated it may resume limited purchases of US soybeans and energy products. Despite this temporary relief, most tariffs remain in place, and no progress was made on larger issues such as Taiwan or Russia. Recent US comments about potential nuclear testing have also added tension.

Figure 1 – China is the global leader in Rare Earth Elements production

2. The Fed rate cut, and the end of quantitative tightening

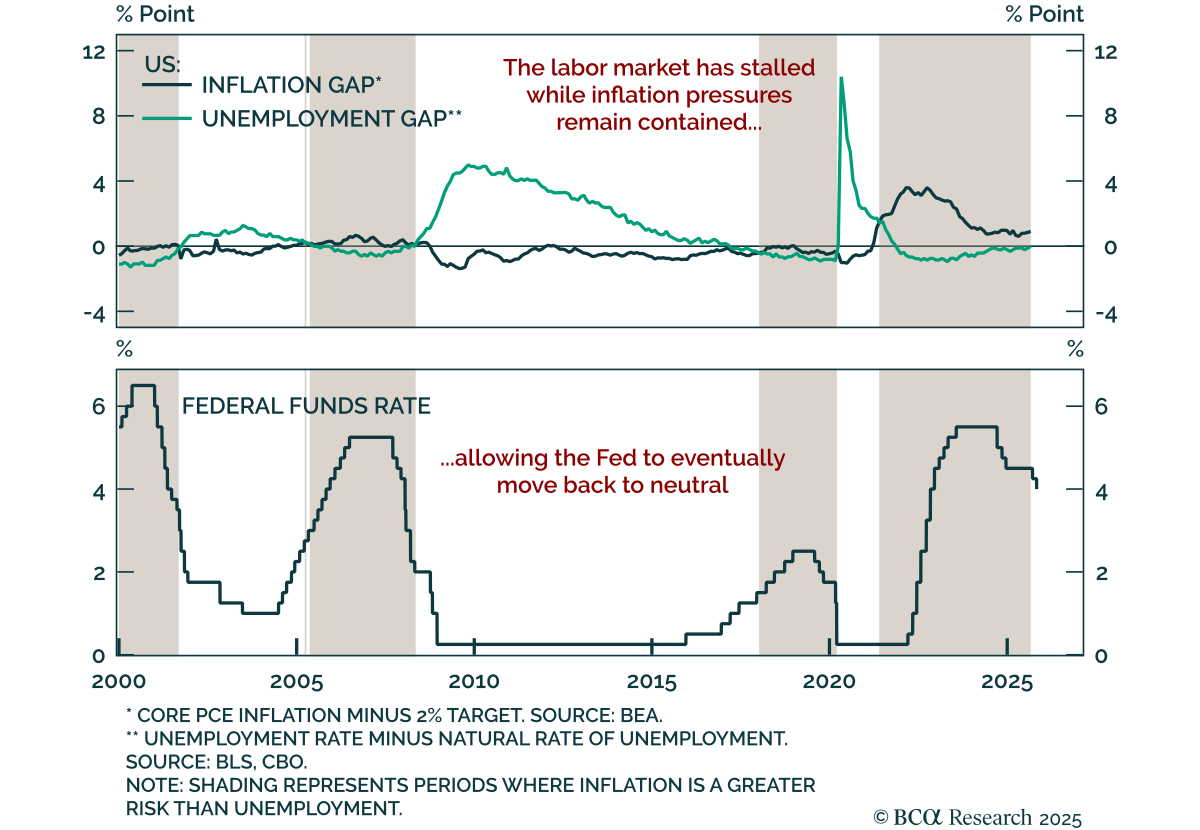

The Federal Reserve lowered its policy rate by another 25 basis points to a range of 3.75 – 4.00 percent. Furthermore, it announced that it will end its balance sheet reduction initiative on December 1st. While these decisions were largely expected, the growing division of opinions within the committee is a point of concern. Fed Chair Jerome Powell cautioned that another cut in December should not yet be considered a guarantee but suggested the decision will be anchored around the neutral rate level, assuming inflation and labour remain controlled – see Figure 2.

Figure 2 – Powell has described the Fed’s policy aim as “modestly restrictive”

Man versus machine

The conventional hope would assume that the lower rate environment will feed through into the economy and subsequently incentivise firms to start hiring again. But, as we’ve already seen, the current status quo regarding capital flows is disproportionately weighted to investment in AI, servers/data centres, and automation infrastructure. Human hiring appears to be last on the list for big corporations. The “wait-and-see” approach to hiring that many companies have taken in 2025 could be justified as a natural response to the business cycle. On the other hand, it is also reasonable to suggest that the capital spending on AI by the hyperscalers has effectively provided a trickle-down and lower-cost alternative for the rest of the private sector, allowing firms to now automate functions that might otherwise have required additional employees.

But for economic activity to remain robust, consumption is essential. Consumption depends on disposable income for households, which in turn relies on an active labour market. Instead, the current trend suggests that corporate priority is going to continue favouring automation over workforce expansion:

- UPS has cut roughly 48,000 jobs so far in 2025, about 34,000 operational roles plus 14,000 corporate positions.

- Amazon has announced layoffs totalling around 14,000 employees at the corporate level, as it reallocates resources toward AI and automation initiatives.

- OpenAI is reportedly hiring over 100 former investment bankers at rates near $150 per hour to train AI models that could replace many tasks currently performed by junior analysts, effectively automating entry-level investment banking work.

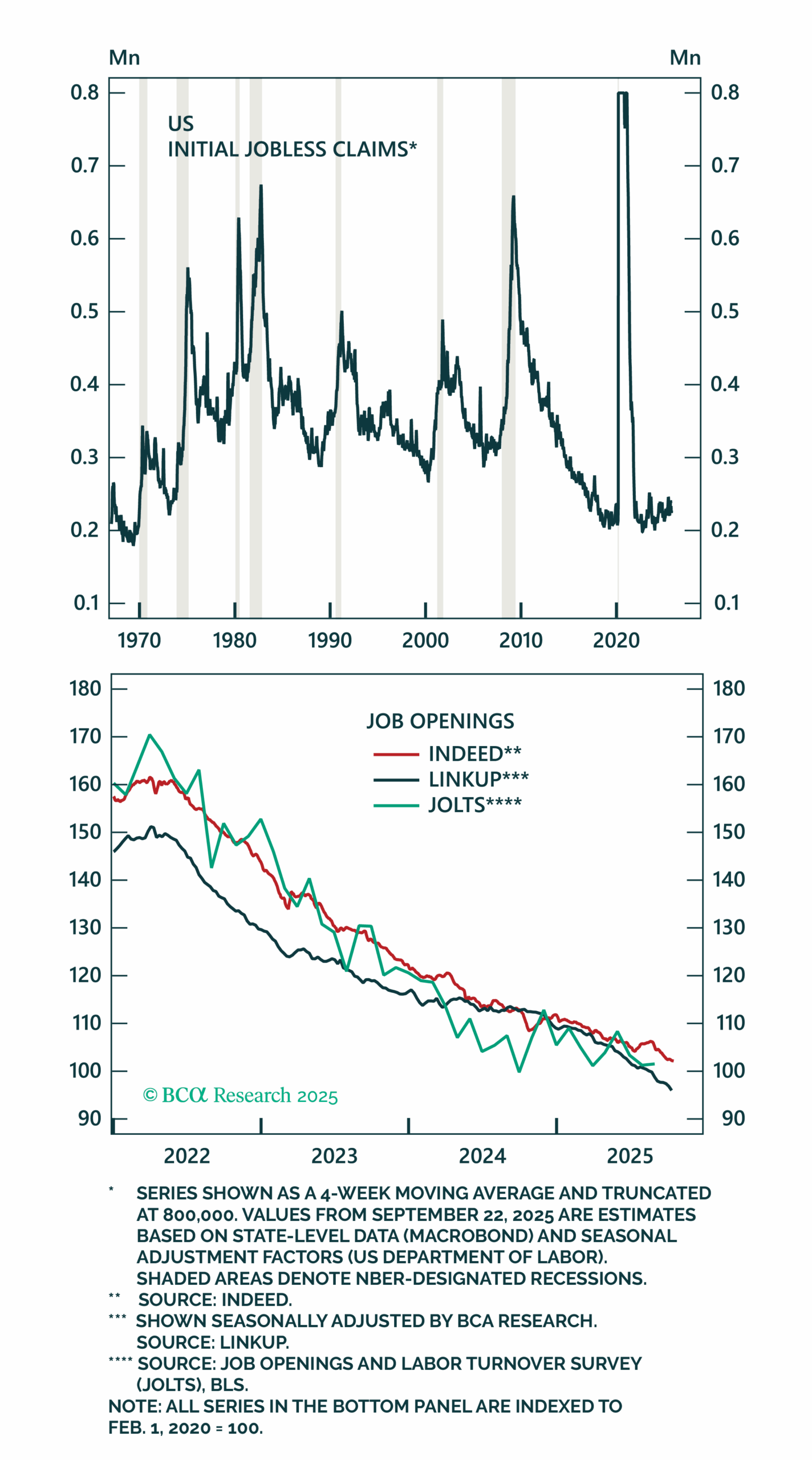

Notably, the market has almost unanimously rewarded these decisions, pricing valuations higher on each news piece. Taken together, these trends raise the question of whether the Fed’s easing will translate into a material boost in jobs, or simply help keep the AI train humming. For now, unemployment has not reached danger levels, however, the lack of new job openings remains on a concerning trajectory – see Figure 3.

Figure 3 – Initial jobless claims remain stable, but real-time job opening indicators continue to trend downward

Three market catalysts to watch

As markets run higher, investors are looking for signs that enthusiasm may be reaching a peak. Three catalysts could serve as early signal posts that valuations are stretching to their limit: Corporate credit, AI capex, and shares representing pure-play speculation.

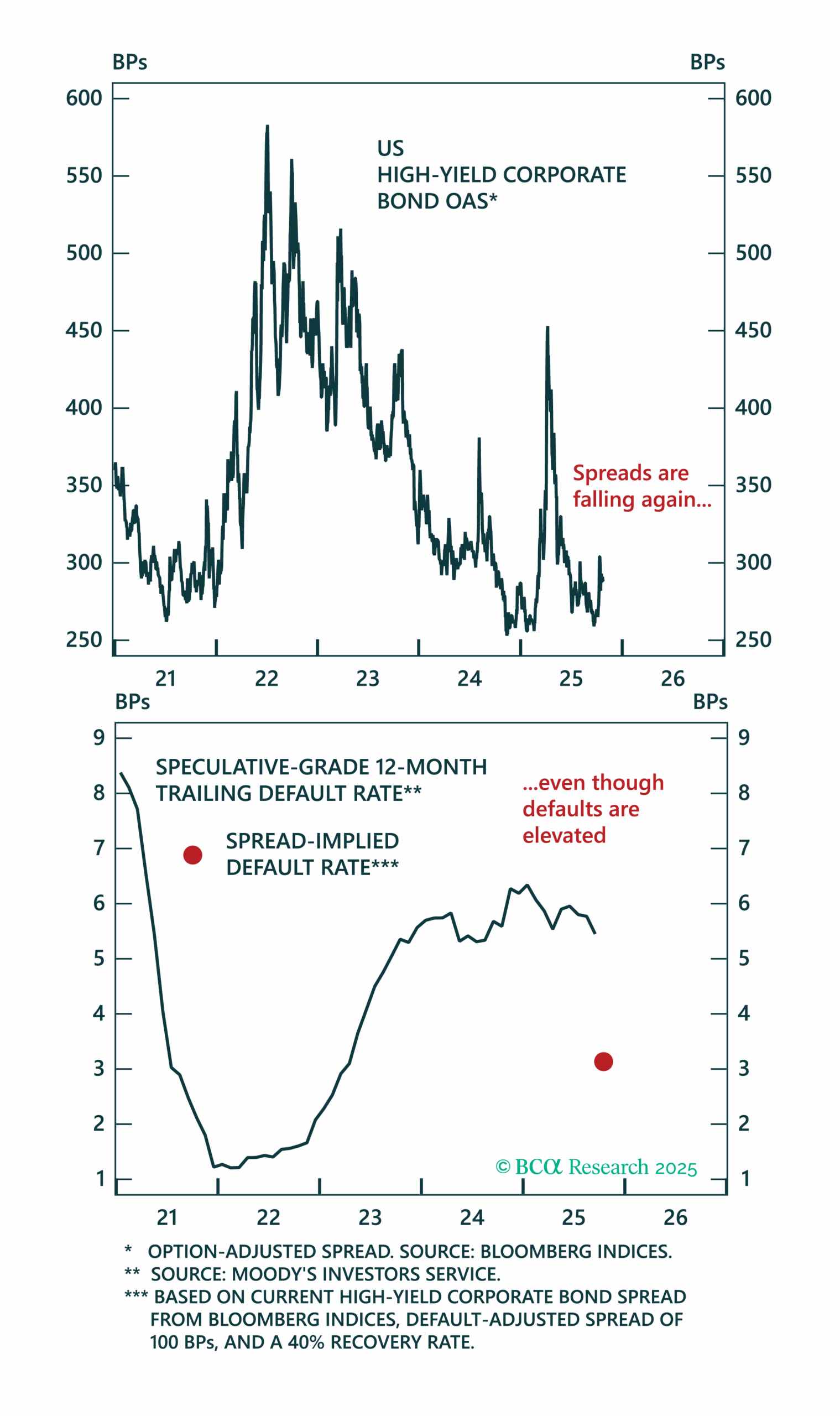

1. Corporate Credit: Spreads tighten despite rising defaults

High-yield credit spreads widened briefly after the notable bankruptcies of Tricolor and First Brands, but have since narrowed. The US high-yield default rate has increased to 5.5%, from 1.2% in early 2022. Despite this, credit spreads have instead fallen about 70 basis points. Current valuations assume this default spike will revert, which may be overly optimistic if economic conditions do not improve – see Figure 4.

Figure 4 – High-yield spreads remain muted despite bankruptcies of Tricolor and First Brands

2. AI Capex: A trade priced for perfection

Optimism around AI is well-founded, but valuations have long already priced this to utter perfection. Bain & Co. estimates AI-related firms would need about $2 trillion in new annual revenue by 2030 to justify current and planned investment.

As mentioned in our prior synopsis, the signal post for this catalyst may mirror the telecom buildout of the late 1990s. Once capex guidelines start decelerating, the trade could quickly lose momentum. Free cash flow among major cloud and chip firms is already slipping, hinting that the peak pace of investment may be near. Like the telecom crash, when the music (capex) stops, so could the foundation that holds up AI valuations – see Figure 5.

Figure 5 – Falling telecom free cash flow was a key precursor to the dot-com bubble bursting

3. Investing in pure speculation

The success of the AI trade has fuelled a certain mentality of speculation-driven investing, with investors all the more seeking to find “the next big topic”. Take quantum computing: Many “pure‑play” firms in this space have little to no revenue and expect losses for years to come. For example, Rigetti Computing posted just $1.5 million in revenue for Q1 2025 and an operating loss of $21.6 million, with even insiders acknowledging that usable quantum systems remain a decade or more away. Despite this, a well-timed investment in the stock 6 months ago would have netted an investor several multiples of return. The current investing playbook appears to be directing attention into areas that are less about fundamentals and dangerously close to “gambling” on the next big tech name.

In parallel, investors have also gone into paranoia about missing the potential regime shift in energy via nuclear shares. For instance, Oklo Inc. has surged in value on the back of this narrative. The company still reports no meaningful revenue, and its first commercial deployment also remains years away.

The recent pullback in some of these names suggests that some sanity is prevailing in capital allocators at the fringes of this trade – see Figure 6. However, if we continue to see frequent new all‑time highs in quantum, nuclear, rare‑earth, and other speculation‑heavy shares, that itself could be a major warning sign that the market is veering into euphoric territory.

Figure 6 – The recent pullback suggests that some rationality is prevailing at the fringes of tech

Investment takeaway

The US economy enters November with mixed signals. Credit and speculative tech valuations remain stretched, and the “AI perfection trade” looks fragile as free cash flow begins to slow. The market’s resilience endures, but the need to monitor for cracks in the façade has become increasingly more important.

Overall, it may benefit to focus on quality assets with already proven cash flows at attractive valuations. Those investing purely on the fear of missing the next train, may find that by the time they climb aboard, the engine has already run out of coal.

If you are interested in finding out more about how cognisance of the macroeconomic backdrop impacts our investment decision making process, connect with Integrity Asset Management and let us help you navigate your investing journey.

For more information on this synopsis or to discuss solutions provided by Integrity Asset Management, please contact us at:

Tel: (021) 671 2112

Cell: 072 513 2684 / 084 601 1025

E-mail: nic@integrityam.co.za / herman@integrityam.co.za

Source: Bloomberg, 31 October 2025